The use of decentralized exchanges (DEXes) has skyrocketed this year, with volumes deposited going from under $1B in January, to surpassing $10B in the past few months.

Automated market makers (AMMs) like Uniswap, Balancer and Curve account for a significant portion of that. These rely on liquidity providers (LPs) — people and entities committing their capital in liquidity pools to facilitate trades and lower slippage. In return, LPs obtain trading fees paid by users.

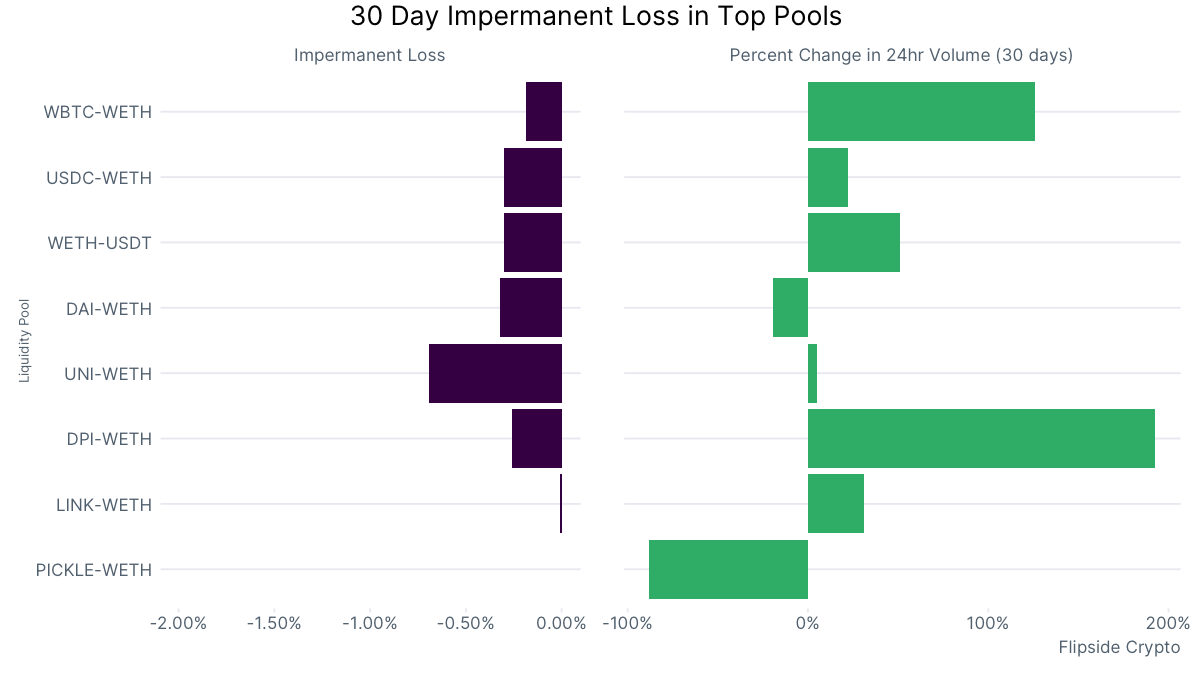

The Fear of (Im)permanent Loss

As with anything in crypto, large price fluctuations present a risk for investors, who continuously buy as the price drops and sell as the price rises. The bet they are making is that there will be enough back-and-forth trades to generate fees that compensate for the losses.

The bar graph above illustrates what investors need to consider: (1) impermanent loss, i.e. the expected volatility and drift of the trading pair; and (2) trading fees as a percentage of pool size.

We focused on the largest pools in terms of volume deposited that have existed for at least 30 days. These all belong to Uniswap, which is an AMM that provides liquidity based on a very deterministic formula. It holds no money of its own, but can raise money from decentralized investors who then share the profits.

Investors are required to supply an equivalent value of the two assets in the pool they choose. For example, if they supply $100 worth of ETH in the ETH-DAI pool, they also have to supply $100 of DAI.

But this ratio is going to change following movements in the market. Impermanent loss refers to how much investors would lose at a current point in time if they withdrew their money from a pool where the price of one of the assets went down. This loss becomes permanent as soon as investors withdraw their funds.

Still, There Is a Clear Incentive for Providing Liquidity

Uniswap allows for the trading of ETH and ERC-20 tokens, and charges a 0.3% trading fee on all its pools. So in order to not get rekt, most liquidity providers pick a pool that presents the most demand (the higher the volume, the higher the fees it generates), and the lowest risks.

It therefore makes sense to see WBTC (wrapped BTC) – WETH (wrapped ETH) at the top, with a total volume of 895MM USD, since those are the two largest blockchains in terms of market cap.

The second largest pool is USDC (Coinbase’s stablecoin)-WETH (wrapped ETH) with 663MM USD in total balance. Pools that include a stablecoin and an asset that is likely to increase are especially desirable, because they are the most likely to generate a profit.

Most pools that are currently at the top are seeing an increase in daily volume.

A Promising New Yield Farming Token: $DPI

DPI-WETH’s 24h volume increased by nearly 200% in the past month. DPI stands for DeFi Pulse Index, which was launched in September 2020 as a permissionless index of the very best DeFi tokens. The idea is that by buying DPI, users can get exposure to a curated set of DeFi projects without paying gas fees for each.

The index has 10 DeFi tokens: LEND, YFI, COMP, SNX, MKR, REN, KNC, LRC, BAL and REP. That order is arranged from the largest portion of the index (LEND at 18.3%) to the smallest (REP at 1.63%).